Getting Started

TaxTron has been designed, by Canadians for Canadians, to allow the

user to prepare their personal Canadian tax returns quickly and easily.

Able to handle returns from simple to complex, Federal, Quebec and Alberta

returns, electronic filing or the traditional printing and mailing of

your return, the program has been engineered to maximize your refund,

getting you the best refund you deserve.

Licensing

and Activation

Professional users must purchase a license prior to obtaining the software.

Upon attempting to print or NETFILE the first return for your clients,

you will be prompted to activate the software using your license number.

This license number is linked to your EFILE number, and different EFILE

numbers require corresponding unique license numbers.

For the personal user, TaxTron is free to

download and prepare your returns. However, you must purchase a license

in order to print or NETFILE a return, unless

your total income is $31,000 or less or you are a full-time student for

at least 4 months as noted on your T2202A tuition form. If the software

has not been activated and a license is required, it will automatically

ask for the license information when attempting to print or NETFILE

a return.

Note: Under CRA guidelines, there is a limit

of 20 returns per machine that can be filed by individuals, either by

print or electronically, regardless of the number of returns prepared.

Professional users are registered with CRA and not subject to these limits.

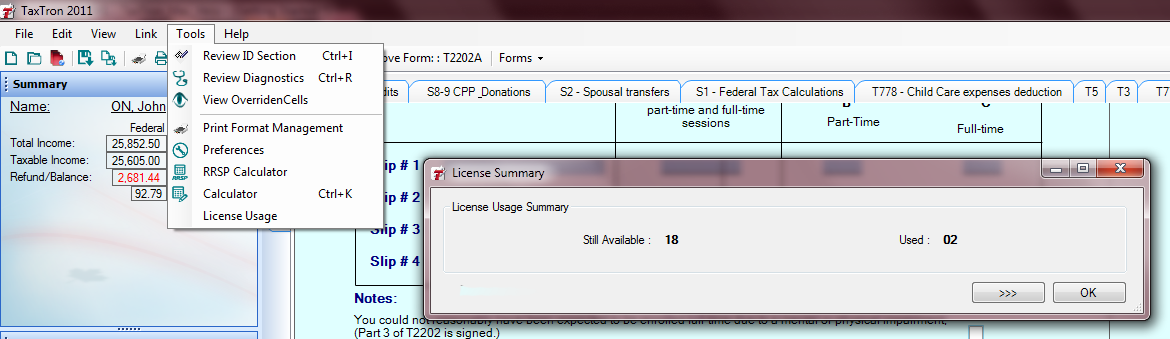

To review your license usage in

TaxTron for Windows®,

go to the Tools menu and select License Usage. Note that professional

users have no limit on usage so this option does not appear in the Professional

software.

Help and Support

Our TaxTron support staff are ready to assist you. Should you have questions

or require assistance, you can contact us by several methods:

E-Mail

Phone

What's

New in TaxTron

New Optimization Feature

- This new option goes through the return, analyzing it for

possible tax savings in order to maximize your return. Pooled

registered pension plan (PRPP) (lines 115, 205,and 208) – The

PRPP is a new retirement savings option for individuals, including

those who are self-employed. For more information about the PRPP,

click here

Other

income (line 130) – Enter on line 130 amounts (grants) paid

to you as a result of taking time away from work to cope with the

death or disappearance of your child because of an offence or probable

offence under the Criminal Code. Adoption

expenses (line 313) – For adoptions finalized in 2013 and subsequent

years, the adoption period has been extended. The adoption period

begins

either when an application is made for registration with a provincial

or territorial ministry responsible for adoption (or with an adoption

agency licensed by a provincial or territorial government) or

when an application related to the adoption is made to a Canadian

court, whichever is earlier; and ends when an adoption order

is issued by, or recognized by, a government in Canada

for that child or when the child first begins to reside permanently

with you, whichever is later.

Donations

and gifts (line 349) – For the 2013 to 2017 years, you may

be able to claim a first-time donor’s super credit.

For 2013

to 2017, if you are a first-time donor, you can claim up to $1,000

of donations of money made after March 20, 2013, for the FDSC.

This credit is calculated by multiplying these donations by 25%.

This is in addition to the credit already allowed for these same

donations that you and your spouse or common-law partner (if you

have one), have claimed on line 340 of Schedule 9.

To qualify as a first-time donor, neither you nor your spouse or

common-law partner, (if you have one), can have claimed and been

allowed a charitable donations tax credit for any year after 2007.

If you have a spouse or common-law partner, you can share the

FDSC, but the total combined donations claimed cannot exceed $1,000.

Investment

tax credit (line 412) – Eligibility for the mineral exploration

tax credit has been extended to flow-through share agreements entered

into before April 1, 2014. Tax

related to the non-purchase of replacement shares in a Quebec labour-sponsored

fund (line 418) – You may have to pay a special tax if you

re deemed your shares from a Quebec labour-sponsored fund to participate

in the Home Buyers’ Plan (HBP) or the Lifelong Learning Plan (LLP),

but did not purchase replacement shares within the prescribed time.

Overseas

employment tax credit (line 426) – From 2013 to 2016, the overseas

employment tax credit will be phased out. It will be eliminated for

2016 and subsequent years. For more information, see Form T626, Overseas Employment Tax Credit. CPP

Revocation - Added option to allow for ability to revoke CPP

Election from Form CPT20, Election

to Pay a Contribution to the Canada Pension Plan. Foreign

property – Under certain circumstances, the reassessment period

for a return has been extended. Under proposed changes, this reassessment

period is extended from three years to six years if:

you did not report income from

a specified foreign property on your return; and you did

not file Form T1135 on time, or you did not identify specified

foreign property, or you identified it incorrectly, on Form T1135.

|