Getting Started

TaxTron has been designed, by Canadians for Canadians, to allow the

user to prepare their personal Canadian tax returns quickly and easily.

Able to handle returns from simple to complex, Federal, Quebec and Alberta

returns, electronic filing or the traditional printing and mailing of

your return, the program has been engineered to maximize your refund,

getting you the best refund you deserve.

Licensing

and Activation

Professional users must purchase a license prior to obtaining the software.

Upon attempting to print or NETFILE the first return for your clients,

you will be prompted to activate the software using your license number.

This license number is linked to your EFILE number, and different EFILE

numbers require corresponding unique license numbers.

For the personal user, TaxTron is free to

download and prepare your returns. However, you must purchase a license

in order to print or NETFILE a return, unless

your total income is $31,000 or less or you are a full-time student for

at least 4 months as noted on your T2202A tuition form. If the software

has not been activated and a license is required, it will automatically

ask for the license information when attempting to print or NETFILE

a return.

Note: Under CRA guidelines, there is a limit

of 20 returns per machine that can be filed by individuals, either by

print or electronically, regardless of the number of returns prepared.

Professional users are registered with CRA and not subject to these limits.

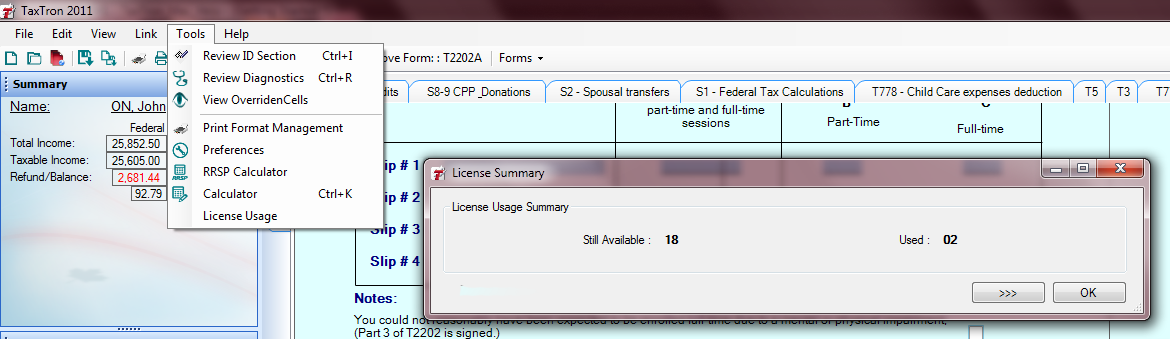

To review your license usage in

TaxTron for Windows®,

go to the Tools menu and select License Usage. Note that professional

users have no limit on usage so this option does not appear in the Professional

software.

Help and Support

Our TaxTron support staff are ready to assist you. Should you have questions

or require assistance, you can contact us by several methods:

E-Mail

Phone

What's

New in TaxTron

Family Tax Cut -

A new non-refundable tax credit of up to $2,000 for eligible couples

with minor children based on the net reduction of federal tax that

would be realized if up to $50,000 of an individual's taxable income

was transferred to the individual's eligible spouse or common-law

partner. This would take advantage of a spouse's lower income tax

bracket. Childrens' Fitness Credit

- This has been increased from $500 to a maximum of $1,000

per child for fees paid in 2014 relating to the cost of registration

or membership for your or your spouse's or common-law partner's child

in a prescribed program of physical activity. Search and Rescue Tax Credit

- The federal government has added a new tax credit for qualified

search and rescue volunteers. Amateur Athlete Trusts

- A new field (Schedule 7, Box 267) has been added for income that

is contributed by an individual for an amateur athlete trust (AAT)

and to allow the income to qualify as earned income for the purposes

of determining the registered retirement savings plan (RRSP) contribution

limit of the trust's beneficiary. T626 Overseas Employment

Tax Credit - The specified percentage for an employee’s qualifying

foreign employment income in determining the employee’s OETC is reduced

to 40% (if no tick in box 6769) and the maximum qualifying foreign

employment income eligible for the OETC is reduced to $40,000. Safety Deposit Boxes

- Fees for the rental of safety deposit boxes are no longer claimable

under carrying charges on line 221. Ontario Community Food

Program Donation Tax Credit - A new non-refundable tax credit,

the community food program donation tax credit for farmers (FC), to

encourage Ontario farmers to donate fresh surplus food has been added.

The claim is 25% of the fair market value of the total qualifying

donations made to an eligible community food program in the tax year,

or in any of the five preceding tax years. The qualifying donations

must be included in the donations claimed for the federal and provinical

charitable donation tax credits for the year the credit is claimed. Manitoba Community Enterprise

Development Tax Credit- The community enterprise development

tax credit (CEDTC) was extended to December 31, 2019. Alberta Royalty Tax Credit

- The Alberta Royalty Tax Rebate carryover is no longer valid for

2014 and subsequent tax years.

|